As we begin 2019, I suggest it prudent we take a look at emergent and critical issues facing massage therapists.

Insurer Discourages Customers from Utilizing Massage Therapy Benefits

At the end of 2018, we witnessed another ploy by Greenshield Canada (GSC) to discourage its customers from using their massage therapy benefits. This bait-and-switch tactic positioned as a moral dilemma was designed to engender guilt – if I use my paid-for benefits to utilize massage therapy, then I’m taking GSC’s resources away from paying for expensive pharmaceutical treatments. In effect, I’m denying someone else care if I consider my own.

Greenshield makes it clear they don’t think much of massage therapy, despite it being one of the most sought-after and used benefits their plans offer.

“Sure, we all love a good massage. It’s relaxing, it soothes our sore muscles, and sometimes (just sometimes) it’s as good as a really good nap. But on the hierarchy of health needs, we’re going to go out on a very well-researched limb and say that massages fall significantly below life-sustaining miracle drugs.” https://www.greenshield.ca/en-ca/news/stories/the-elephant-in-the-waiting-room?fbclid=IwAR3PzUjhXxE7e1umgKS2aAVobiWAODBmhKCG7TCiAn6-hZuBo7j-tUxi4HU

Never mind that the Ministry of Labour cites MusculoSkeletal Disorders (conditions RMTs can positively affect) costing employers hundreds of millions of dollars affecting tens of thousands of citizens https://www.labour.gov.on.ca/english/hs/pubs/pains/index.php

GSC appears to dismiss these conditions in favour of resource-intensive conditions affecting far fewer citizens.

Insurer Threatens Removal of MT Benefits

In another post We Spend More on Massage Than Mental Health Services…Time for a Change?, GSC propose dropping massage therapy coverage as part of a SmartSpend initiative.

“Massage. GSC’s most popular and costly paramedical service is removed as a core benefit in order to re-invest significant funds in the more serious health challenges noted above.”

GSC via the Toronto Star took opportunity to criticize chiropractic and physiotherapy as well as massage therapy in a 2015 article https://www.thestar.com/business/personal_finance/2015/04/13/the-rise-of-the-three-amigos-of-health-care.html?referrer=https%3A%2F%2Fwww.google.ca%2F.

It appears GSC is increasingly hoping to discourage customers from making claims against insurance products customers have paid for. Read my rebuttal here https://www.massagetherapycanada.com/opinion/report-on-health-benefits-use-misses-the-point-2569

Clearly there’s a conflict of interest here…the company that takes in the premiums can boost revenues by discouraging or denying claims. Is it OK for the fox to guard the hen-house?

I sympathize with Greenshield’s cost concerns. They must take in premiums from their customers, then cover operational and marketing costs, staff and executive salaries before they cover claims.

Certainly, in the current system there is ample opportunity for waste and abuse. However insurance may be an outmoded and expensive way of reimbursing health care services…there’s a lot of money paid in premiums not directly benefiting GSC’s customers.

Health spending accounts and government tax credits put the money in your hands, and pressure health care providers to be diligent with their treatment plans. Supplementing tightly-controlled provincial health plan spending with these accounts/credits might better address the needs of Canadians, while keeping everyone involved accountable.

Insurer Believes People are Like Automobiles

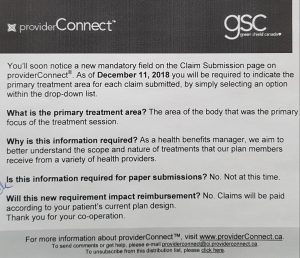

Another area to watch related to GSC, the concept of sectional therapy. GSC announced they will now be collecting data on the primary treatment area. This may be the harbinger to future claims approval linked to treating only the symptomatic areas of the body, rather than considering global bio-mechanical dysfunctions or the body-mind / psycho-social connection for the whole person.

Another area to watch related to GSC, the concept of sectional therapy. GSC announced they will now be collecting data on the primary treatment area. This may be the harbinger to future claims approval linked to treating only the symptomatic areas of the body, rather than considering global bio-mechanical dysfunctions or the body-mind / psycho-social connection for the whole person.

People would be treated like automobiles – replacing a muffler, changing a tire – instead of the complex human beings we are. GSC claims adjudicators without health care credentials or an assessment of the individual would be determining breadth and scope of care.

We should ask, “Are insurers part of the health care system? If so, what guides their decision-making processes when approving or denying care claims?”

Is there a threat to RHP self-regulation?

A recent Globe & Mail article is critical of the chiropractic regulator https://www.theglobeandmail.com/…/article-calls…/… The authors maintain the regulator is not doing enough to stem false or exaggerated claims made by their member practitioners.

Tim Caulfield, research chair of health law and policy at U of A has been an outspoken critic of self-regulation for naturopathic practitioners. https://www.cbc.ca/…/researcher-wants-oversight-of…

Caulfield questions whether granting regulation to professions without rigorous evidence gives the public a false sense of confidence.

In “Self-Regulation is shielding bad doctors, not protecting patients” the Toronto Star editorial board state “Once again, doctors have shown they can’t be relied on to properly regulate their own profession. It’s time for the provinces to force the matter through legislation that more clearly defines what it really means to regulate the practice of medicine in the public interest.” https://www.thestar.com/…/self-regulation-is-shielding…

It appears that every year at the RMTAO AGM, the CMTO registrar shares that self-regulation for RHPs is uncommon now in most countries, and its days may be numbered in Ontario.

Given what we are seeing in these other professions, what do you think is the future is for RMTs and self-regulation?

Media Coverage for Misconduct Allegation Increasingly Sensationalist

Media coverage for allegations of misconduct by RMTs contains strong authority images (police cars, badges), cites allegations not yet proven, and rarely mentions MT as a regulated health profession.

https://www.massagetherapycanada.com/regulations/are-rmts-disproportionately-vulnerable-to-allegations-of-sexual-misconduct-4169

If MT was Infused into Publicly Funded Health Care, Would We Be Ready to Serve?

This year representatives from the Registered Massage Therapists’ Association of Ontario (RMTAO) petitioned government to consider MT in health care applications for individuals with chronic pain, palliative care and home care. https://secure.rmtao.com/default.asp?id=1151&article=103

If the wish was granted, and MT were able to work in these integrated health settings:

Are RMTs prepared and properly trained to work with contemporary western medicine practitioners in these integrated settings?

Can we expect service fees to drop to WSIB and auto-insurance service fee levels (about 30-40% below RMTAO’s recommended fee schedule)?

Would you be prepared to work at that level of pay?

What other regulatory and operational requirements would accompany the privilege of working in the system?

What other issues do you see emerging? How would the issues listed here affect your day-to-day practice?

Please post your comments below

There is another issue I feel is finding it’s way into sabotaging the public’s view of who massage therapists are and that is the practice of insurance companies asking their clients to RATE THEIR THERAPIST. Sun Life has recently integrated this practice when a claim is submitted after a treatment. They ask the client to rate their therapist by offering a number of stars ( no subjective questions are even asked, no criteria to keep in mind, nothing) just offer some stars. THEN a recommendation for the client to try a different therapist next time (a name is given) as they would be “cheaper”! There are several issues that present a problem here and I don’t know if RMTs fully understand the impact to their practice if this is allowed to go on uncontested. (1) Rating a trained RMT with no criteria, no critical reasoning that can be evaluated or improved upon or be proud of offers ZERO value to client and therapist alike and I find it insulting that we can be thought of as no more than a menu item! It can also seriously impact one’s practice in a multi practitioner setting. For example, if you are given 4 stars (again, based on what who knows) but your coworkers all get 5 stars, Sun Life clients may reasonably assume that something is amiss with the 4 star therapist and would rather book with the 5 star people. But what if 4 stars are offered because they don’t direct bill? What is 4 stars are offered because the client ran out of benefits at time of appointment and are now angry that they had to pay? There could be many reasons for that rating but when if is not asked to clarify, how can a therapist answer or try to correct? (2) The practice of suggesting an alternate therapist based on what they charge is also highly questionable and unfair to the therapist. What if the treatment offered involved premium out of pocket supplies ? What if the average cost of a massage therapy session is determined by geography? Again, no reasons are offered just suggestions based on keeping costs down, I suppose. I’m sure there are more detriments to this type of marketing fo consider but fue biggest one, is the therapists ability to opt of this type of marketing. No permission was ever asked of us to be included and there is no option (that I can see) to not be included. Even if you do not direct bill, the client will be asked to offer stars that can then be looked up by other prospective clients. My opinion is that this seems demeaning to healthcare practitioners ( RMTs are NOT targeted exclusively) and gives the general public a poor view of our worth when we can be rated and compared to one another when no criteria is offered to substantiate the general impression.

Great point Edie! I support patient/client feedback on session/treatment plan experience, but as you point out, the insurer provides no variables in rating a practitioner and this may be interpreted unfairly or pejoratively, or may affect the ability for practitioners to bill for services. A conniving attempt to discredit practitioners and reduce claim submissions. This will be an essential point in the larger discussion of insurer relations. Thanks for posting!